Shining a Bright Light on Shadow Payroll

Recently, I presented a webinar with the GPMI on the topic of Shadow Payroll.

It was surprising how many payroll professionals registered and attended on the day. To me, this indicates that although Shadow Payrolls are not well understood, there is a strong desire within the global payroll community to continue to learn more about them. Let’s follow up from the webinar and reinforce some of the key points that were covered during the presentation.

Last month I found myself in a conversation with a manager of US payroll in a well-known international company. She shared that it seems to take 20 x more effort to process payroll for one of their 300 expatriates than for any of their 60,000 other employees.

Whether it is 10 x, 20 x, or 100 x, it seems whenever the topic of expatriate payrolls come up, eyes roll, stories pour out, and you can feel that certain pain that anyone who has managed expatriate payrolls knows well.

The focus of this article will be to cover these main pain points:

- What makes expatriates so hard to process?

- Can the complexity be explained?

- Can it be simplified?

There are 2 attributes that are responsible for shadow payroll complexity and corresponding frustrations for payroll processors.

1. The first complication relates to international assignment policies, which gets to why we are doing this in the first place. Expatriates are covered by mobility policies that are meant to address important concerns such as:

-

- Taxes,

- Cost of living,

- Housing,

- Foreign exchange,

- And even whether the employer will spring for relocating pets.

These policies are often designed by human resources professionals trying their best to be fair to the employee and employer. But when putting these policies together, the last thing HR is thinking about is how they will be reflected in payroll.

Payroll staff, tasked with processing expatriate payrolls that need to interpret and reflect these policies, are often unfamiliar with the logic of the transactions they are being asked to administer.

There is no context for them to work with so setting up the pay codes and executing the transactions is like putting a bicycle together from its pieces without knowing exactly what it is supposed to look like at the end.

2. Second, there are process complications.

Because expatriates are often on both home and host payrolls at the same time, there is a need to coordinate a regular exchange of payroll information between two countries.

Each period of earnings, deductions, and taxes must be properly reported:

- On two payrolls

- In two currencies,

- Often at two payroll frequencies

- While ensuring that net pay is delivered timely and accurately.

This requires a solid understanding of what should be reflected on each payroll, what to gross-up, and which payroll is delivering each element of compensation or benefit. All of this needs to be managed according to the rules of home and host law, as well as company mobility policy and accounting protocols.

This article will shed some light on these 2 aspects of expatriate payroll. However, it is only a starting point as there are all kinds of variations on the themes presented.

I’ve chosen to use a US outbound expatriate program for purposes of my illustrations as based on webinar attendees, I expect that the readers of this article are primarily US payroll professionals.

In order to begin to break down expatriate program policy logic and explain the basics of the underlying payroll processes, let’s start with three quick definitions.

1. Shadow Payroll

- When an employee transfers abroad on an expatriate assignment from the US, “Shadow Payroll” refers the host country payroll and it is primarily used to report earnings, deductions, and taxes in the host location currency. It may deliver local allowances (like the cost of living allowances), but it generally does not deliver net pay to the employee. This is done via the home (US) payroll.

2. Expatriate

- As relates to this article, an expatriate

- is an employee who is transferring on a long term assignment from the US to another country

- is covered by a company-sponsored mobility policy

- remains on the US payroll in addition to the Shadow Payroll throughout the duration of the assignment

3. Long Term Assignment

- A long term assignment is one that will last long enough that payroll reporting is statutorily required in the host country (you can assume longer than six months) and the assignment is not indefinite (i.e. the employee is not taking up a permanent residence in the host country).

At this point you might be asking yourself:

“Why do we have to report expatriates on two payrolls in the first place? Wouldn’t things be so much simpler if we could just pay them out of one – the US or the host country – rather than both?”

The answer is “Absolutely yes”. It would be much simpler to pay an expatriate out of one payroll. But there are good reasons that expatriate payrolls are often structured as “split payrolls”.

Consider first that an expatriate usually expects to return to the US after a couple of years.

Therefore s/he would likely want to remain tied to US FICA and Medicare programs, and, possibly, maintain their participation in certain US benefits like 401(k). Additionally, there may be US equity or bonus programs that the employer wants the employee to participate in that may not be available if the expatriate is employed solely in the host country. And our long-term expatriate is almost always tax resident and required to be reported on the host country payroll in the same way that you can’t just transfer a German national to work in a US subsidiary and pay them out of Germany without legally setting them up on a US payroll as well while they work here.

These ends can only be achieved if the expatriate is reported on both the home (US) payroll in addition to the host payroll.

Assuming, then, that a split payroll is a preferential structure for an expatriate employee, let’s look at the basics of global mobility policy and consider how it will affect the setup of US and Shadow payrolls through this lens.

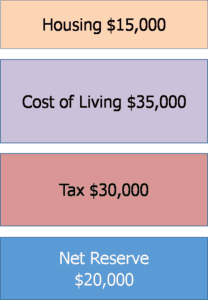

The “Balance Sheet”

Although there are an endless variety of ways to do it, a common approach for developing expatriate policies is referred to as the “Balance Sheet” model.

To be clear, the Balance Sheet has absolutely nothing to do with accounting.

Instead, it refers to a method that addresses 4 specific factors of economic life while an expatriate is on assignment, and how through a series of allowances, those factors can be “balanced” in a way where the expatriate’s net pay and quality of life can be protected.

The 4 economic factors are:

- Housing

- Cost of Living

- Tax

- Net Reserve

The theory is that any employee receiving compensation spends it on the first three factors leaving the fourth, net reserve for things like savings, retirement plans (including 401(k) and social security), or other personal, non-essential purchases like hobbies.

The balance sheet theorizes that for any combination of salary, family size and status, and home location a theoretical housing cost, cost of living and tax cost can be determined to leave a specific net pay that the employee would have been receiving at home. The example I used in my recent webinar for an individual earning $100,000 follows:

The balance sheet model suggests that when the expatriate goes on the assignment they would be concerned that

- Their net remains the same ($20,000) and

- That their quality of life remains consistent

Let’s think about this for a moment.

What if the employer reduced the amount paid to the employee via the US payroll and only delivered the employee $20,000 net. And further, the employer agreed to provide appropriate housing to the employee in the assignment location, a cost of living allowance in an amount that would allow the employee to replicate his or her stay-at-home lifestyle, and also paid 100% of any tax (either in the US and/or in the assignment country).

In that case, the employee’s economic life would be “in balance”. S/he would have the same net after tax in the bank while enjoying an equivalent housing and quality of life while on assignment.

This is the basis of the balance sheet model.

Translating the Balance Sheet into Payroll Structure & Transactions

How this gets reflected in payroll transactions in its purest form is as follows:

- In the example above, continue paying the employee $100,000 gross via the US payroll (you need to keep the $100,000 salary intact on the payroll to ensure that benefits keying off salaries like pension, 401(k) or GTL are calculated off the correct amount)

- Set up NEGATIVE taxable earnings to reflect the stay at home amounts that are not to be delivered to the expatriate on the US payroll (e.g. hypothetical housing, hypothetical cost of living, hypothetical tax). This should leave the employee receiving $20,000 net via the home (US) payroll.

| Compensation | Annual | Semi-Monthly |

|---|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The $20,000 net reserve should be grossed up as the employee has, theoretically “paid” his/her tax obligation through the Hypo Tax. The US pay structure each period should then look like this:

| United States | |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please note: I have condensed the salary and offsetting hypotheticals into a single net number for simplicity in this illustration.

Shadow Payroll

On the Shadow Payroll side, the Net Reserve reported and paid in the US plus the company funded gross-up are to be reported in addition to any locally paid allowances like ACTUAL housing costs (e.g. rent) and local-currency cost of living allowance paid to replicate the same theoretical basket of goods and services the employee is presumed to have purchased at home. Those amounts are grossed up on the Shadow Payroll which covers all host country tax costs.

Using the UK as the example of the host location as I did in my recent webinar, the host reporting looks like this assuming annual UK rent of £26,915 and an annual cost of living allowance of £34,6

| SHADOW (UK) | |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In this example, I have assumed that

- The US payroll runs twice monthly and the Shadow Payroll only monthly

- Two pay periods of US Net Reserve and US Grossup are reported on the monthly UK payroll

- The US Net Reserve and US Grossup are translated to GBP at .769 GBP/USD

- One month’s rent (26,915/12) has been paid to a landlord directly

- One month’s cost of living (34,605/12) is delivered to the expatriate in GBP via the UK (Shadow) payroll

- The UK gross-up rate is 35%

- The US transactions are in blue and the UK transactions are in green

Note that all of the US items are reported in addition to amounts locally paid via the Shadow. And also note the non-taxable deduction of £1,387.84 (circled in red above). This ensures that the US paid amounts (net reserve plus US gross-up) are not double paid by the UK payroll.

Following the running of the Shadow (UK) payroll, the US payroll must pick up the transactions that were locally executed and gross them up in the US as well. See below:

| United States | |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Again, the blue transactions represent US payroll deliverables and the green amounts are those translated from the UK (Shadow) payroll and reported on the US payroll. The Shadow payroll allowances and gross-up have been translated at 1.3 USD/GBP. Note here as well that there is a non-taxable deduction to ensure that the Shadow-delivered amounts (housing, Cost of Living and UK tax gross-up), are not accidentally double-paid through the US payroll.

The UK amounts will only be reflected in one US payroll in the succeeding month. The second US payroll will be “clean” (only net reserve and gross-up reported) as all the Shadow pays have been properly reflected on the first US payroll of the succeeding month.

The cycle then repeats itsel

Best Practices

In closing, here are some best practices relating to setting up and operating US/Shadow payrolls:

- Careful coordination between home and host country payrolls to share payroll data each period is critical

- Set up a non-taxable deduction code to offset the reporting of taxable income first reported on the foreign payroll

- Work with a finance department to set up specific rules about the application of foreign exchange rates so that you don’t need to try and figure this out each period

- Ask tax advisor if you should shut off US Federal Income Tax withholdings to avoid excessive US tax gross-ups

- Also, ask your tax advisor if US state gross-ups are required for an expatriate on a state-by-state basis

- There may be items that are excludable in one country but taxable in the other (like contributions to retirement plans). Ask your tax advisor to identify

Conclusion

This topic is complex and often not well understood – the article only scratches the surface of mobility policies, split (shadow) payroll structure and a sample set of transactions.

This summary aims to give some insights into the logic behind shadow payrolls and a map as to how to begin to set up and operate them within your global payroll shop.